You may be looking for alternative ways to preserve your wealth and pass it on to your beneficiaries. Here are three options you might consider.

Roth Conversion

If you are willing to pay income taxes now instead of your beneficiaries paying them later, you could convert your IRA to a Roth IRA. Anyone can convert a traditional IRA to a Roth IRA. However, you generally have to include the amount you convert in your gross income for the year of conversion. In addition to having to pay taxes on the amount converted, the beneficiaries of your Roth IRA will generally have to liquidate the account within 10 years of inheriting it, but they won’t pay federal income taxes on the distribution(s).

Life Insurance

You could take distributions from your IRA and use them to buy life insurance on your life. The beneficiaries you name in the life insurance policy will receive those proceeds tax-free at your death. The policy beneficiaries could use the tax-free proceeds of the life insurance to pay any income taxes they would owe on the balance of the IRA they inherit from you. Or, if you’ve been able to liquidate or spend down your IRA during your lifetime, the tax-free life insurance death benefit would replace some or all of the taxable IRA that otherwise would have been inherited by the beneficiaries.

Irrevocable Trust

You could create an irrevocable trust and fund it with non-IRA assets. An irrevocable trust can’t be changed or dissolved once it has been created. You generally can’t remove assets, change beneficiaries, or rewrite any of the terms of the trust. Often, life insurance is used to fund the irrevocable trust. You can direct how and when the trust beneficiaries are to receive the life insurance proceeds from the trust after your death. In addition, if you have given up control of the property, all of the property in the trust, plus any future appreciation on the property, is removed from your taxable estate.

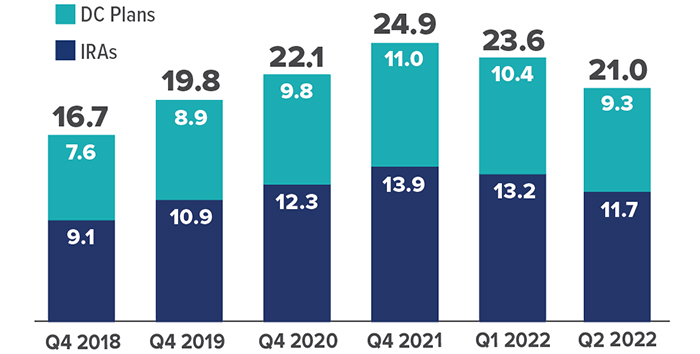

Wealth Cache

Assets held in individual retirement accounts (IRAs) and defined-contribution plans such as 401(k)s dipped in the first half of 2022 to $21 trillion. Even so, that total was up more than 25% from year-end 2018.

U.S. retirement assets, in trillions

Source: Investment Company Institute, 2022

While trusts offer numerous advantages, they incur upfront costs and often have ongoing administrative fees. The use of trusts involves a complex web of tax rules and regulations. You should consider the counsel of an experienced estate planning professional and your legal and tax professionals before implementing such strategies.

As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. In addition, if a policy is surrendered prematurely, there may be surrender charges and income tax implications. Any guarantees are subject to the financial strength and claims-paying ability of the insurer.

To qualify for the tax-free and penalty-free withdrawal of earnings, a Roth IRA must meet the five-year holding requirement, and the distribution must take place after age 59½ or due to the owner’s death, disability, or a first-time home purchase ($10,000 lifetime maximum). Under current tax law, if all conditions are met, the Roth IRA will incur no further income tax liability for the rest of the owner’s lifetime or for the lifetimes of the owner’s heirs, regardless of how much growth the account experiences.