Unfortunately, you can’t take a tax-free withdrawal of just after-tax money, leaving any taxable amounts in the account for later. All the assets in your traditional, SEP, and SIMPLE IRAs must be aggregated, which means they are treated as one pool of money, even if they are held at different financial institutions. The pro-rata rule is sometimes called the “cream in the coffee rule” because once you combine after-tax dollars (“the cream”) with pre-tax dollars (“the coffee”) in one of your IRAs, distributions from any of them will have an inseparable mix of both. (Roth and inherited IRA assets are excluded.)

You should consider the potential impact of the pro-rata rule well before you intend to retire or begin taking any taxable IRA distributions — or undertake a Roth conversion — as there may be worthwhile opportunities to help blunt its impact.

Doing the Math

Here are the steps involved in calculating the taxable portion of an IRA distribution.

Step 1: Total the balance of all IRAs required to be aggregated (SEP, SIMPLE, and traditional IRAs) as of December 31 of the year the distribution was taken.

Step 2: Add the amount of all distributions (and conversions) taken during the same calendar year.

Step 3: Total the after-tax dollars (or basis) in those IRAs. The basis includes nondeductible IRA contributions and/or after-tax 401(k) contributions rolled over to an IRA.

Step 4: Determine the pro-rata percentage of after-tax dollars by dividing the Step 3 amount by the Step 2 amount.

Step 5: Calculate the nontaxable portion of your calendar-year distributions by multiplying the Step 4 percentage by the amount of the distribution. The remainder of the distribution is taxable income.

Let’s say that Peggy, who recently retired, takes distributions totaling $25,000 from her traditional IRA. That account has a balance of $300,000 at the end of the same year, and her after-tax basis in the IRA is $100,000. She also owns a SEP IRA, which has a balance of $200,000 and no after-tax funds, so the basis in that account is zero, and her combined IRA balance is $500,000. Calculating Peggy’s pro-rata percentage of after-tax dollars ($100,000 ÷ $500,000 + $25,000 = .19) determines that 19% of her distribution will be tax-free. Therefore, the nontaxable portion of her calendar-year distributions ($25,000 x .19) is $4,750, and the amount of taxable income is $20,250. This hypothetical example of mathematical principles is used for illustrative purposes only.

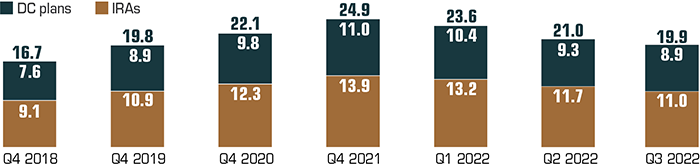

Wealth Cache

Assets held in IRAs and defined-contribution plans such as 401(k)s dipped in the first three quarters of 2022 to $19.9 trillion.

U.S. retirement assets, in trillions

Source: Investment Company Institute, 2022

Isolating the Basis

You may be able to lessen the impact of the pro-rata rule by reducing the amount of pre-tax IRA dollars by year-end. This is called isolating the basis. If you have access to a workplace plan such as a 401(k) and reverse rollovers are permitted, you might consider rolling pre-tax IRA funds into the plan. You could also use pre-tax dollars to make a qualified charitable distribution or a qualified health savings account (HSA) funding distribution, which is a one-time direct transfer from a traditional IRA to an HSA.

The IRA custodian will not calculate the taxable and nontaxable portions of any distribution. It is up to you to track your IRA basis by filing IRS Form 8606 for every year you make after-tax contributions, convert pre-tax assets to a Roth account, or receive a distribution that is subject to the pro-rata rule.